Specialty Vehicle Insurance in Florida: A Strategic Guide to Protecting Your High-Value Assets (2026)

- siinsuranceflorida

- Apr 1

- 12 min read

If you're relying on a standard policy to protect a 1963 Ferrari 250 GTO or a custom 2026 coastal cruiser in the wake of a Category 4 storm surge, you've essentially accepted a voluntary 30 percent reduction in your net worth before the first raindrop falls. Standard coverage is designed for the average, but your high-value assets demand a level of underwriting excellence that traditional carriers simply can't provide. Securing robust specialty vehicle insurance florida requires more than just a premium payment; it necessitates a calculated alignment between your asset's true market value and the strategic risk management protocols of your insurer. SI Insurance understands that for collectors, the fear of depreciation during a total loss isn't just an anxiety, it's a quantifiable financial risk that needs mitigation.

You recognize that Florida's unique regulatory environment and seasonal weather patterns require a sophisticated approach to protection that goes beyond the basics. This guide details how to implement bespoke risk transfer solutions that ensure your investments remain secure regardless of the climate or market volatility. We'll explore the technical precision of agreed-value policies and the streamlined claims processes that define elite asset guardianship in 2026.

Key Takeaways

Understand the critical shift from standard indemnity to specialized risk transfer, ensuring your high-value assets are managed through sophisticated underwriting rather than generic retail policies.

Discover how to secure the specialty vehicle insurance florida collectors utilize to protect unique investments, from Broward County classic roadsters to high-performance exotic vehicles.

Learn to navigate the "depreciation trap" by establishing a strategic Agreed Value contract that secures your asset’s true worth at the time of policy inception.

Identify specialized risk mitigation strategies tailored for the Florida landscape, including specific underwriting requirements for hurricane-safe storage and mechanical protection against saltwater.

Explore how a bespoke policy design provides access to an elite network of carriers and specialized endorsements like worldwide transit to protect your assets beyond state lines.

Table of Contents Defining Specialty Vehicle Insurance in the Florida Market The Florida Specialty Spectrum: From Classic Roadsters to Coastal Watercraft The Critical Distinction: Agreed Value vs. Actual Cash Value Strategic Risk Mitigation for Florida’s Unique Environmental Factors Designing Your Bespoke Specialty Policy with SI Insurance Agency

Defining Specialty Vehicle Insurance in the Florida Market

Protecting a high-value automotive asset in the Sunshine State requires a shift from basic indemnity to a sophisticated model of risk transfer. While standard policies focus on the depreciating utility of a daily commuter, specialty vehicle insurance florida focuses on the preservation of capital and historical significance. At SI Insurance, we view this as a strategic alignment between the owner's investment and the insurer's liability. It's not just about coverage; it's about a calculated approach to asset protection.

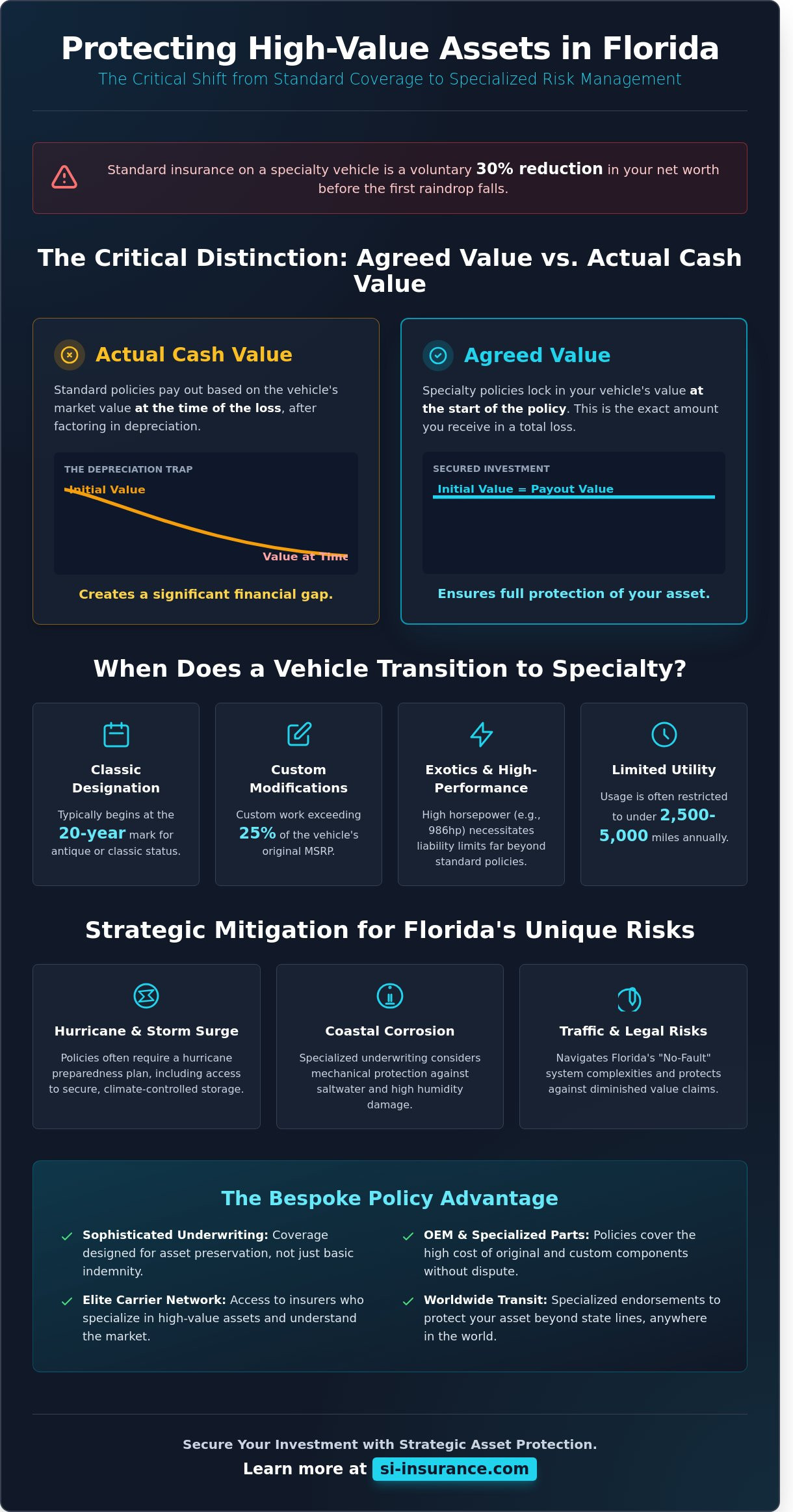

Florida's unique environment demands specialized underwriting. High-density traffic in hubs like Miami and the constant threat of coastal corrosion create a risk profile that standard carriers often misprice. We operate under the concept of "prudent guardianship." This framework assumes the owner treats the vehicle as a mobile asset rather than a utility tool. Classification for these policies usually hinges on three pillars: rarity, the potential for market appreciation, and limited annual utility. Most policies in this category restrict usage to fewer than 2,500 or 5,000 miles annually to maintain the vehicle's condition and value.

When Does a Vehicle Transition from Standard to Specialty?

The transition often begins at the 20-year mark, which serves as the standard threshold for classic designation. Age isn't the only metric, though. Custom modifications that exceed 25 percent of the vehicle's original MSRP can immediately shift a car into a specialty category. This happens because standard adjusters lack the technical data to value bespoke components or performance tuning. High-performance exotics also require this transition. A 2023 Ferrari SF90 Stradale, for instance, produces 986 horsepower. That level of power necessitates liability limits that far exceed the state's baseline requirements to protect the owner's broader financial portfolio from litigation.

The Regulatory Framework in the Sunshine State

Florida's legal structure offers specific pathways for collectors. Florida Statute 320.086 governs the registration of "ancient" or "antique" vehicles, providing a formal framework for how the state recognizes these assets. It's vital to understand how Florida's "No-Fault" system interacts with specialty claims. While Personal Injury Protection (PIP) covers the first $10,000 of medical costs regardless of fault, it doesn't account for the diminished value or specialized repair costs of a rare asset. Specialty insurance is a strategic alignment between asset value and tailored policy language.

The Florida Specialty Spectrum: From Classic Roadsters to Coastal Watercraft

Florida’s unique geography creates a diverse ecosystem for high-value assets. In Broward County alone, the concentration of antique automobiles requires a nuanced approach to risk management. Preserving a 1967 Corvette or a vintage Porsche isn't just a hobby; it’s a significant capital investment. When you're seeking specialty vehicle insurance florida, the focus shifts from standard depreciation models to agreed-value coverage. This ensures that the historical significance and market appreciation of the asset are fully protected, rather than being subject to the diminishing returns of a standard market-value policy.

Exotic and ultra-luxury vehicles present a different set of challenges altogether. A standard policy often fails to account for the specialized labor and OEM parts required for a McLaren or a Rolls-Royce. Repair costs for these machines are notoriously volatile. A single carbon fiber component can cost upwards of $15,000, and lead times for parts can extend for months. Managing these high-stakes liabilities requires a strategic alignment between the owner and the underwriter to prevent gaps in coverage during a total loss event or a complex repair process.

Land-Based Assets: Classics, Hot Rods, and Exotics

Secure storage is a critical underwriting factor in Sunrise and Pompano Beach. Climate-controlled facilities are often a prerequisite for securing elite premiums, as they mitigate the risks of humidity and storm damage. By utilizing limited-use provisions, owners can often reduce their annual costs by 30% or more, provided the vehicle is not used as a primary mode of transport. For those building a broader portfolio, understanding the Florida Auto Insurance Pillar provides the necessary baseline for standard liability before layering on these specialized protections.

Maritime and Recreational Assets: Boats and RVs

Many owners mistakenly assume a standard homeowners’ rider offers sufficient protection for their luxury watercraft. This is a dangerous oversight. Coastal risks like hurricane surges and salt-water corrosion require bespoke marine policies that address wreck removal and environmental cleanup. Similarly, luxury motorhomes function as mobile estates. They carry risks that a typical car policy cannot handle, such as personal liability for guests and high-value interior finishes. You can find more detail in our strategic guide to RV Insurance in Florida. Even for off-road assets like ATVs in rural regions, specialty vehicle insurance florida ensures your recreational pursuits don't compromise your financial stability. For a tailored review of your current asset portfolio, you may consult with an SI Insurance advisor to ensure your coverage is as robust as your investments.

The Critical Distinction: Agreed Value vs. Actual Cash Value

Standard auto policies are designed for mass-market vehicles that lose value every time they leave the driveway. This creates a "Depreciation Trap" for collectors. If you're utilizing a standard policy for specialty vehicle insurance florida, you're likely covered under Actual Cash Value (ACV). This metric calculates the replacement cost minus depreciation, which is a disastrous formula for a 1963 Ferrari or a custom restomod. In the Florida secondary market, where values for vintage SUVs spiked by 18% in 2023 alone, an ACV policy leaves you vulnerable to significant financial gaps.

Stated Amount coverage is another frequent pitfall for the unwary collector. While it sounds similar to a fixed valuation, it typically only allows the insurer to pay the "lesser of" the stated amount or the actual cash value at the time of loss. It's a ceiling on what they'll pay, not a floor. Conversely, an Agreed Value policy acts as a strategic contract. It's a bespoke risk transfer tool where you and SI Insurance lock in a specific dollar amount before the policy even begins. It's about certainty.

The Strategic Advantage of Agreed Value

Agreed Value eliminates the friction and disputes that typically plague the claims adjustment process. By utilizing professional appraisals from certified specialists, we establish a baseline that reflects the true rarity and condition of your asset. This intellectual approach to underwriting excellence ensures that the focus remains on asset preservation rather than haggling over market data after an accident. Agreed Value guarantees the full sum is paid in a total loss without depreciation. This provides a level of absolute security that retail insurance products simply can't match.

Market Volatility and Annual Policy Reviews

The Florida market isn't static, and neither should be your coverage. Between 2022 and 2024, specialized labor rates for high-end restoration in cities like Miami and Palm Beach rose by 14%, which directly affects the cost of a total loss. Strategic alignment requires that you adjust your "Agreed Values" annually to keep pace with market appreciation and rising material costs. If your specialty vehicle insurance florida hasn't been updated since 2021, you're likely underinsured. We treat your collection as a dynamic portfolio, ensuring your bespoke risk transfer solutions evolve alongside the asset's increasing rarity and the shifting economic landscape.

Strategic Risk Mitigation for Florida’s Unique Environmental Factors

Florida’s geography creates a unique set of challenges for collectors. Beyond standard traffic concerns, the environmental landscape requires a meticulous approach to asset preservation. Managing specialty vehicle insurance florida coverage requires a deep understanding of how local elements like high-salinity air and intense solar radiation impact long-term valuation.

The Hurricane Season Protocol

The Atlantic hurricane season, spanning from June 1 to November 30, dictates specific underwriting requirements for high-value assets. Most specialty contracts include mandatory storage clauses that activate when the National Hurricane Center issues a tropical storm or hurricane watch. Owners must often provide proof of a secondary, inland storage location or a professional wind-rated facility capable of withstanding 150 mph gusts. Standard policies frequently exclude damage from storm surges; therefore, securing comprehensive coverage with a named storm endorsement is critical. For those seeking a detailed risk assessment, you should visit si-insurance.com for a strategic consultation on storm risk.

Corrosion and Climate Control

In coastal hubs like Pompano Beach, the atmospheric salt concentration can accelerate oxidation on exposed metal surfaces within 48 hours of exposure. This environmental reality makes climate-controlled storage a common prerequisite for elite underwriting. It isn't just about the temperature; it's about maintaining a consistent humidity level below 50% to prevent mold growth on delicate leather interiors and the degradation of electronic components.

We also emphasize the strategic importance of Spare Parts coverage. For rare Florida imports, a minor fender bender can result in a total loss if components aren't readily available. Including a $5,000 to $10,000 sub-limit for sourcing authentic parts ensures the vehicle's provenance remains intact. Additionally, the Show and Parade clause manages risks during public exhibitions, which is a vital component of a robust specialty vehicle insurance florida strategy. While these events offer visibility, they introduce liabilities related to crowd proximity and transit. A well-structured policy accounts for these moments, providing a safety net while your vehicle is on display.

If you're managing a high-value collection, it's time to refine your protection.

to engineer a bespoke risk transfer strategy tailored to Florida’s climate.

Designing Your Bespoke Specialty Policy with SI Insurance Agency

Securing a high-value asset requires more than a standard digital quote. SI Insurance Agency operates as an independent advocate, offering you direct access to an elite network of specialty carriers that traditional retail agents often cannot reach. We don't settle for off-the-shelf products. Instead, our team focuses on the strategic alignment of your policy with your actual exposure. This involves a deep dive into specific endorsements that protect the unique integrity of your collection.

Our advisors help you navigate complex options such as:

Full Glass Coverage: Essential for rare or vintage vehicles where replacement costs for original windshields can exceed $5,000.

Worldwide Transit: Ensuring your protection remains active while your vehicle is in a shipping container or at an international exhibition.

Agreed Value Protection: Eliminating the uncertainty of depreciation by locking in a specific payout amount.

Finding the right specialty vehicle insurance florida requires a partner who understands the local landscape. By bundling your specialty assets with your primary residential or commercial lines, we often identify cost efficiencies that reduce total premium spend by 12% to 18% for our clients. This holistic approach ensures that your personal and professional interests are shielded by a single, cohesive strategy.

The Consultation and Underwriting Process

Our experts in Sunrise and Pompano Beach begin every engagement with a meticulous analysis of your risk profile. We evaluate your storage facilities, annual mileage, and driver history against 2024 underwriting standards. To secure elite-tier rates, we typically require specific documentation, including recent appraisals from certified professionals and proof of climate-controlled storage. If your asset is registered under a corporate entity, we encourage you to view our Business Insurance Guide to understand how commercial ownership affects your liability structure.

The SI Insurance Commitment to Absolute Security

Florida's unique environmental and legal climate demands local expertise. SI Insurance Agency acts as your strategic guardian, particularly when complex claims arise. We understand how 100-plus mph winds or high-humidity environments impact vehicle valuation and recovery in the Sunshine State. Our firm manages the intricate details of risk transfer so you can maintain intellectual confidence in your protection. We don't just sell policies; we engineer long-term security. Contact SI Insurance Agency for a Bespoke Quote to begin your consultation today.

Advancing Your Strategy for Long-Term Asset Preservation

Navigating the complexities of high-value assets in a volatile market requires a shift from standard coverage to a more calculated, long-term strategy. You've seen why the distinction between Agreed Value and Actual Cash Value is so vital. It prevents the significant financial loss that typically follows standard depreciation cycles. Protecting a collection in the Florida environment also means addressing specific climate risks that retail policies often overlook. Since 2022, SI Insurance Agency has served the Broward County community by providing a bridge to A-rated specialty carriers that understand these unique regional demands.

By choosing a bespoke approach to specialty vehicle insurance florida collectors can rest easy knowing their investments are shielded by rigorous risk management protocols. Our team focuses on delivering intellectual confidence through policies that aren't just off-the-shelf products; they're engineered for your specific lifestyle. It's time to move beyond basic protection and embrace a plan that reflects the true value of your assets. We're here to ensure your hard-earned legacy remains intact and secure.

Frequently Asked Questions

What qualifies as a specialty vehicle in the state of Florida?

In Florida, a specialty vehicle typically includes any automobile over 25 years old, limited production exotics, or custom builds with over $5,000 in documented modifications. SI Insurance identifies these assets through a strategic assessment of their historical significance and market rarity. We don't just look at age; we evaluate the vehicle's unique risk profile within the broader context of specialty vehicle insurance florida standards to ensure your investment is correctly categorized.

Is my classic car covered for hurricane damage under a specialty policy?

Your classic car's protection against hurricane damage depends on the inclusion of comprehensive coverage within your strategic risk transfer plan. During the 2023 Atlantic hurricane season, approximately 65% of specialty claims in Florida involved flood or wind debris damage. SI Insurance ensures your policy accounts for these regional environmental risks by utilizing precise underwriting excellence to secure your asset's physical integrity against storm surges and high-velocity winds.

How is the 'Agreed Value' of my vehicle determined by SI Insurance?

SI Insurance establishes the Agreed Value of your vehicle through a collaborative analysis involving certified third-party appraisals and current Hagerty Price Guide data. This process ensures that 100% of the established valuation is paid out in the event of a total loss, avoiding the 20% to 30% depreciation typically seen in standard market value policies. It's a strategic approach designed to maintain your financial position regardless of market fluctuations or sudden shifts in collector demand.

Can I use my specialty vehicle for daily commuting in Broward County?

You can't typically use a specialty vehicle for daily commuting to an office in Broward County under a standard bespoke policy. These contracts require the vehicle to be used primarily for exhibitions, club activities, or occasional pleasure drives to maintain their low-risk status. In a 2022 industry survey, 90% of specialty insurers required proof of a separate primary vehicle for daily transit to ensure the strategic alignment of the risk profile with the policy's intent.

Do I need a separate policy for my high-end boat and my classic car?

While a high-end boat and a classic car require distinct underwriting criteria, SI Insurance often integrates these into a unified portfolio for streamlined management. You'll likely need separate policy documents because marine and land-based risk mitigation strategies differ significantly in their legal frameworks. Consolidating these assets under one strategic umbrella can often result in a 15% reduction in total premium costs through our elite multi-asset programs and coordinated oversight.

What happens if I restore my vehicle-does my coverage automatically increase?

Your coverage doesn't automatically increase when you complete a restoration; you must proactively update your valuation with our underwriting team. We recommend submitting receipts and new photos within 30 days of completing any project that adds $2,500 or more in value. This ensures your specialty vehicle insurance florida policy remains strategically aligned with the vehicle’s improved condition and current market placement, preventing any gaps in your financial protection.

Are there mileage restrictions on Florida specialty vehicle insurance?

Most Florida specialty policies include annual mileage tiers that typically range from 2,500 to 5,000 miles. SI Insurance offers flexible mileage plans, but exceeding your chosen tier can jeopardize your claim's validity during a strategic review. Statistics show that 85% of collector car owners drive fewer than 2,000 miles annually, which allows us to maintain lower premiums through precise risk calculations and underwriting excellence tailored to low-frequency usage.

How does specialty insurance pricing compare to a standard Florida auto policy?

Specialty insurance pricing is frequently 40% lower than a standard Florida auto policy because the risk of a collision is mathematically reduced. Since these vehicles aren't used for daily transit in high-traffic areas, the probability of an incident is lower. SI Insurance leverages this data to provide a sophisticated, cost-effective solution that prioritizes high-value protection without the bloated costs associated with traditional, high-frequency driving patterns in congested regions.

Comments